School fees are vital for the sustainability of educational institutions, as government funding typically provides little contribution to their income. Schools rely on parents to pay their fees in order to maintain operations and uphold the high educational standards that both parents expect and learners deserve. However, collecting outstanding fees can be challenging, particularly when parents face financial difficulties.

It’s crucial to distinguish between a parent experiencing genuine financial hardship and one who is neglecting their responsibilities or deliberately avoiding payment. In the case of hardship, a more empathetic and flexible approach may be appropriate. However, when a parent is intentionally evading payment, a more assertive and strategic approach will be necessary to address the situation effectively.

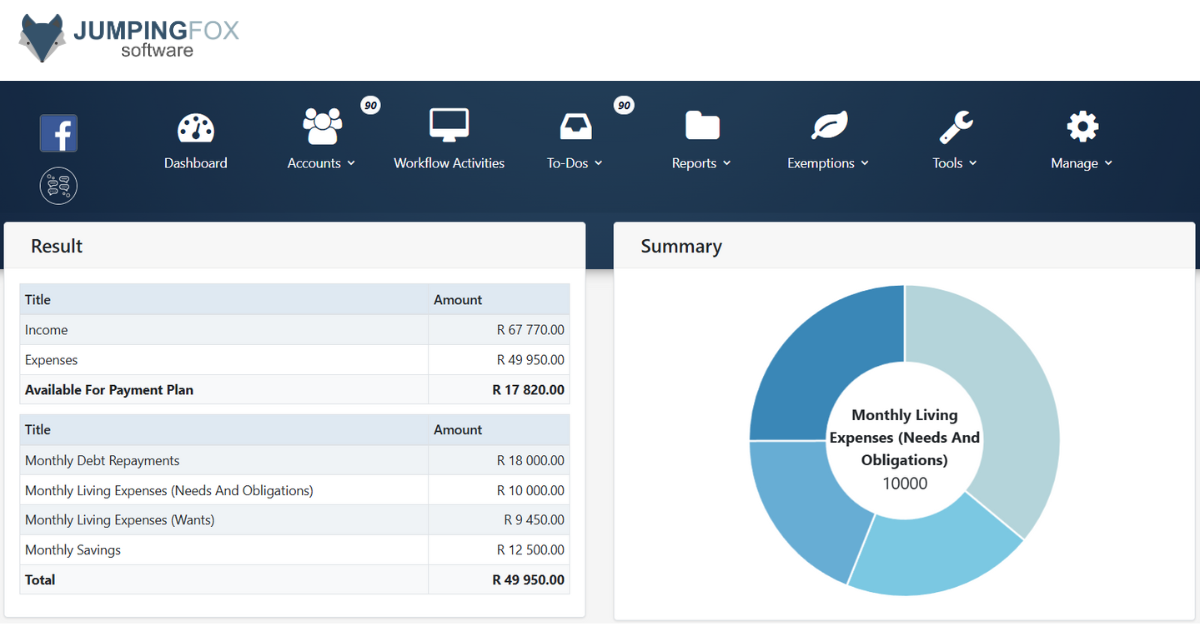

By reviewing a parent’s financial situation through a detailed financial profile, schools can assess the parent’s probability of payment, choose appropriate collection strategies, and improve recovery success.

Financial profiling involves analysing a parent’s income, expenses, assets, liabilities, and credit history to determine their ability to pay. This is an effective alternative to just demanding payment, as it allows schools to take a more informed and empathetic approach, ensuring they are collecting fees from those who have the means to pay.

The Importance of Financial Profiling

Financial profiling is a vital tool in debt collection. It allows you to gather essential information about a parent’s financial situation, including their income, expenses, assets, liabilities, and credit history, which is typically sourced from a credit bureau. This comprehensive approach helps schools assess the likelihood of repayment and choose the most appropriate collection strategy.

Credit bureaus, such as Experian, TransUnion, and VCCB, are organisations that collect and maintain credit information on individuals and businesses. This information includes a person’s credit history, outstanding debts, payment behaviour, and other relevant financial data. By obtaining a credit report from one of these bureaus, schools can gain a better understanding of a parent’s financial situation and their ability to pay. It's important to remember that a credit report can only be acquired with the parent’s consent. However, an excellent alternative is the adverse findings report from VCCB, which is available through debtor management software like Jumping Fox Software. Unlike a credit report, this report does not require the parent’s consent and provides enough information to create a financial profile of the parent. The use of credit and adverse finding reports for financial decision-making are very useful in evaluating someone's ability to repay debts.

By leveraging this data, schools can assess whether a parent has a strong financial profile, which indicates a higher likelihood of paying school fees, or if the parent’s financial situation suggests a lower probability of payment, requiring a different collection strategy.

Why can't I just demand payment of school fees?

One of the primary reasons schools should not immediately demand payment without reviewing a parent’s financial situation is that not all parents can afford to pay their school fees at the moment. Demanding payment without understanding their financial position could lead to strained relationships with parents and wasted resources in futile collection efforts.

Without first assessing a parent’s financial standing, schools risk spending time on strategies that won’t yield results. For example, if a parent is experiencing financial hardship or if their credit report shows signs of significant debt and unpaid obligations, pursuing aggressive collection strategies may be counterproductive. In these cases, offering a payment plan or exemption, in the case of public schools, could yield better results, fostering cooperation and understanding.

Financial Profiling: A Smarter Approach

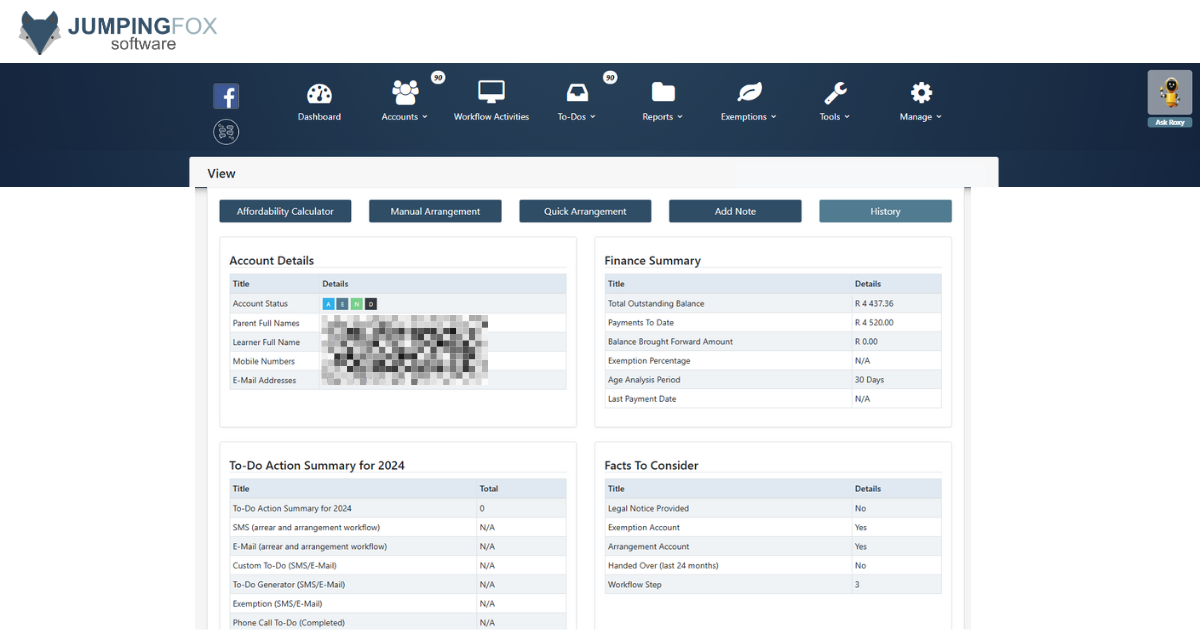

Financial profiling is key to deciding the best course of action in collecting outstanding school fees. Several important factors must be considered, and a credit or adverse finding report from a reputable credit bureau is one of the most effective tools to help schools gather critical financial data. If you use debtor management software, the collection reports it provides can also assist in profiling the parent. These reports track the current year's payment history and record all actions taken in the collection of school fees, offering valuable insights into the parent's payment behaviour and history.

What data to consider when compiling a credit profile:

- Income and Employment Status: One of the first things to assess is a parent’s employment status. A parent with a stable income is more likely to make consistent payments. Conversely, a parent who is unemployed or underemployed may face difficulty paying school fees, regardless of their intentions.

- Assets and Property Ownership: A parent who owns property or significant assets is more likely to have the financial means to pay outstanding fees. This information can often be confirmed through the credit report. According to Experian, 70% of homeowners in the U.S. have a higher likelihood of paying their financial obligations compared to renters.

- Credit History: Credit reports provide a wealth of data on a parent’s financial behaviour. Information about late payments, judgments, or high levels of debt can give schools a sense of the parent’s likelihood of making timely payments. For instance, a report from TransUnion indicates that nearly 30% of adults in South Africa have at least one judgment against them, which may suggest that collecting fees from these parents could be a challenge.

- Debt-to-Income Ratio: Another important aspect of profiling is assessing the parent’s debt-to-income ratio. A high ratio suggests the parent is over-leveraged and may not have the financial ability to pay additional debts. This is an important statistic to verify through the credit report, which typically includes outstanding loans and other debts.

- Exemptions and Payment History: Schools can also review whether the parent has applied for exemptions, especially in the case of public schools. Some credit bureaus, like Experian, provide additional financial indicators that may show whether a parent is eligible for fee exemption or if the parent is currently enrolled in a debt recovery program.

- Debt Recovery Warnings: Credit reports from bureaus often include “adverse” findings, such as debt recovery warnings, which indicate that the person has not paid off significant loans. A judgment or a formal court order is a strong sign that the person may not have the financial means to pay school fees.

How to Use Financial Profiling in School Fee Recovery

Once the financial profile is established, you can decide on the appropriate course of action based on the parent’s ability to pay. A financial profile created using credit bureau data combined with information from debtor management software, such as Jumping Fox Software, offers the insights needed to assess whether a parent is likely to pay their fees in full or if a more flexible approach is necessary.

Scenario 1: High Probability to Pay

If the credit report shows a healthy financial history, such as stable employment, good credit scores, and the ownership of valuable assets, the parent has a high probability of paying school fees. In these cases, communication efforts can remain firm but friendly, reminding the parent of their obligations and encouraging them to settle the fees.

Studies have shown that personalised emails have a much higher chance of resulting in payment, with an open rate of 6 times higher than generic emails, according to Experian. These emails can also include links to easy payment options, further encouraging the parent to settle their debt.

Scenario 2: Low Probability to Pay

If a parent’s financial profile shows low income, significant debt, or poor credit, it is clear that they are unlikely to pay their outstanding fees in full. In these cases, schools should consider offering flexible payment plans, reducing the outstanding balance, or exploring exemption options if the parent is eligible.

Financial profiling helps schools avoid wasting time on aggressive collection strategies that are unlikely to succeed. According to research by TransUnion, about 40% of debtors who are subjected to aggressive collections eventually stop paying altogether. Thus, taking a softer, more empathetic approach can yield better results.

Scenario 3: No Capacity to Pay

For parents who clearly cannot afford to pay, pursuing collections will likely prove fruitless. If the financial profile indicates that the parent has no income or assets, a write-off or exemption may be the most sensible approach.

Moving forward with collections despite a parent’s inability to pay may not only harm the relationship but could also hurt the school’s reputation within the community.

The Benefits of Financial Profiling

- Efficiency in Collection: Financial profiling enables schools to identify high- and low-probability payers, allowing them to allocate resources more effectively. Schools can focus their efforts on accounts with a higher likelihood of successful payment while adjusting their approach for those with a lower probability of paying.

- Data-Driven Decision Making: Using data from credit bureaus ensures that decisions are based on objective, verifiable information, rather than assumptions or biases.

- Preservation of Relationships: Offering flexible options based on a parent’s financial profile can help preserve the relationship with the school, ensuring parents feel understood and supported.

- Reduced Collection Costs: Financial profiling helps avoid wasted resources on non-payers, allowing the school to allocate resources to more effective strategies, such as offering payment plans or exemptions.

Frequently Asked Questions

Conclusion

Optimising school fee recovery is not just about demanding payment, it’s about understanding the parent’s financial situation and using that insight to make informed decisions. Financial profiling, which incorporates data from credit reports, financial indicators, and debtor management software, is an essential tool in assessing a parent’s probability to pay. By leveraging this information, schools can develop fairer, more effective debt recovery strategies, ultimately improving both their fee collection success and their relationships with parents.

Daleen: daleen@jumpingfoxsoftware.com / 021 - 001 4758